The 50/30/20 rule was popularized by Senator Elizabeth Warren in All Your Worth (2005). Two decades later it’s still the cleanest entry point to budgeting — and during my CFP® studies I keep coming back to it as the framework most clients can actually remember.

What does each bucket actually contain?

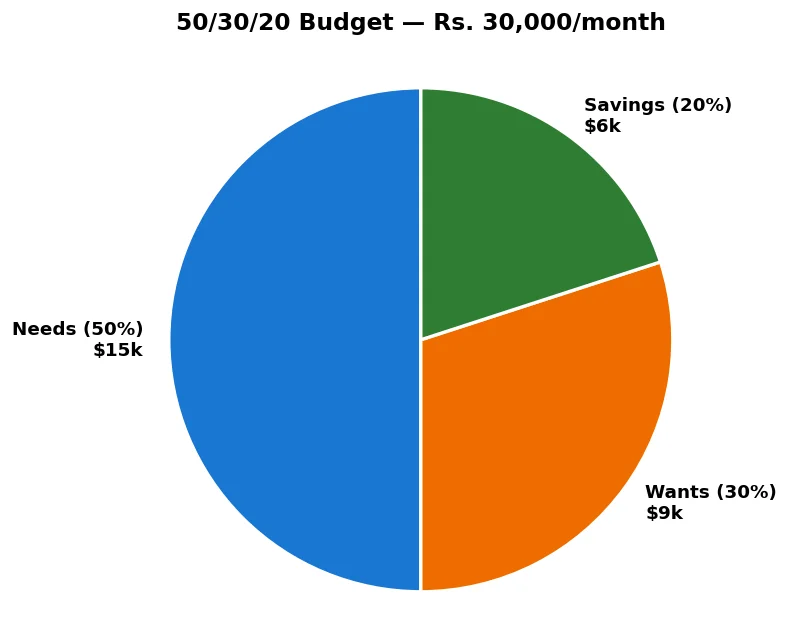

50% — Needs

Stuff you genuinely can’t skip:

- Rent or mortgage + property tax + HOA

- Utilities — electricity, water, gas, heating

- Health insurance premiums + minimum prescriptions

- Groceries (basic, not Whole Foods extravagance)

- Transportation — car loan, gas, insurance, public transit

- Minimum debt payments (student loans, credit card minimums)

- Phone (basic plan)

30% — Wants

- Restaurants, takeout, DoorDash

- Streaming, gym, hobbies

- Travel, concerts, sports tickets

- Clothes beyond replacement basics

- The premium phone plan / unlimited everything

20% — Savings & Debt Payoff Above Minimums

- Roth IRA contributions ($7,000/year limit in 2026 per IRS)

- Extra 401(k) above employer match

- HSA contributions ($4,300 individual limit 2026 per IRS)

- Emergency fund top-ups

- Aggressive credit card / student loan payoff above the minimum

What does this look like on real US salaries?

Approximate after-tax take-home (single filer, 6% 401(k), average state):

| Gross | Net/mo | 50% Needs | 30% Wants | 20% Save |

|---|---|---|---|---|

| $40,000 | ~$2,650 | $1,325 | $795 | $530 |

| $60,000 | ~$3,750 | $1,875 | $1,125 | $750 |

| $85,000 | ~$5,000 | $2,500 | $1,500 | $1,000 |

| $120,000 | ~$6,800 | $3,400 | $2,040 | $1,360 |

| $150,000 | ~$8,300 | $4,150 | $2,490 | $1,660 |

When does the 50/30/20 rule break?

It breaks in expensive metros. A 1BR in Manhattan ran ~$4,500/month in late 2025; in SF ~$3,800; in Boston ~$2,900. On a $75K salary ($4,447 net/month), 50% = $2,223 for ALL needs — already less than rent alone in those cities.

Real fix in HCOL cities:

- Take roommates. Cuts the rent line in half.

- Adjust to 60/20/20 or 65/15/20. Protect savings first, then needs, then squeeze wants.

- Earn more. Sometimes the answer isn’t budgeting harder — it’s that the salary doesn’t fit the city yet.

What about high-debt situations?

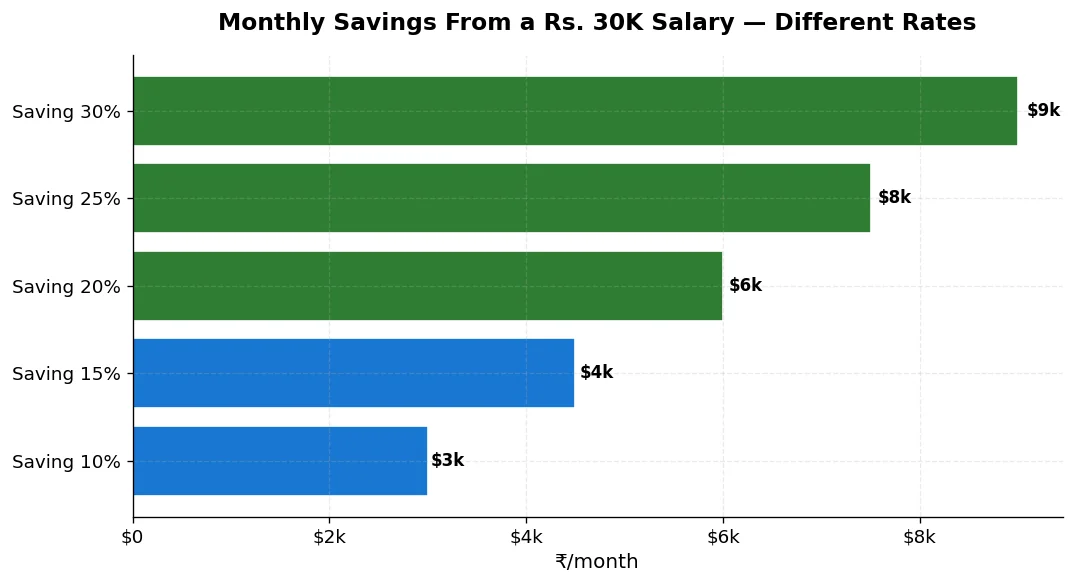

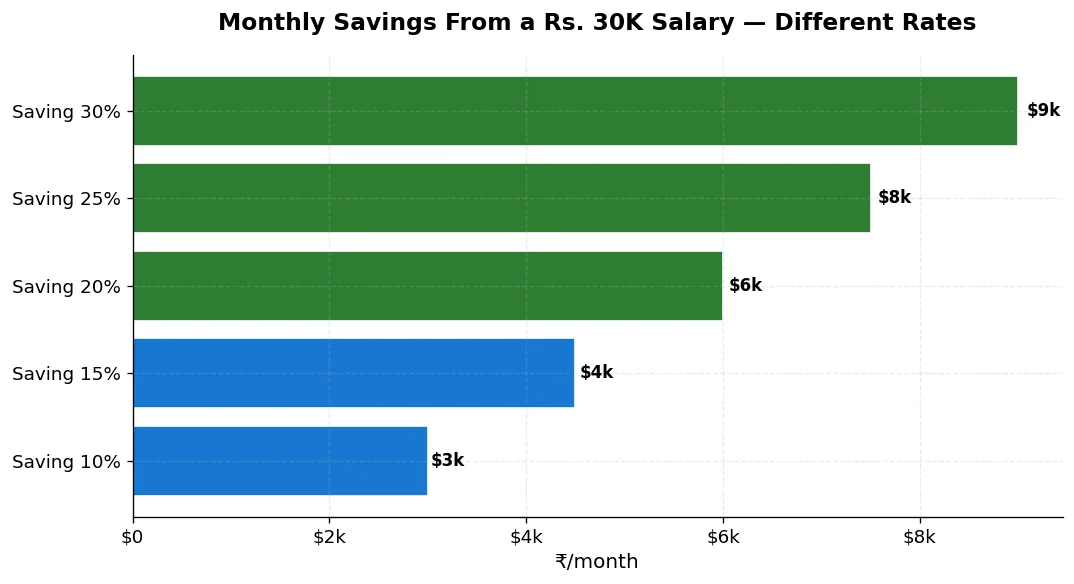

If you’re carrying $20K+ in credit card debt at 22% APR (the 2026 US average per Federal Reserve G.19), flip the rule to 50/20/30 — needs stay at 50%, wants drop to 20%, debt payoff bumps to 30%.

The math: $5,000 of credit card debt at 22% APR, paid at $250/month, takes ~25 months and costs ~$1,290 in interest. At $400/month, ~14 months and ~$675 interest. Aggressive payoff is mathematically a 22% guaranteed return — no investment competes.

How is this different from a zero-based budget?

Zero-based budgets (like YNAB’s system) assign every dollar a job before the month starts — needs/wants/savings each get specific category amounts. 50/30/20 is the macro view; zero-based is the micro view.

Use 50/30/20 to set the percentages, zero-based to allocate within each bucket. They work together.

What counts as a “need” vs “want”?

Honest gut test: could you skip it for 6 months without losing your job, your health, or your housing?

- Gym membership — want (your job doesn’t depend on it)

- Basic groceries — need; Whole Foods premium items — want

- Car payment — need only if you need the car for work; want if it’s a luxury upgrade

- Streaming services — all wants, even the one you “need” for the new season

- Therapy — I’d categorize as a need, full stop

How do you actually implement it?

- Calculate net monthly take-home (after tax, FICA, 401(k), health insurance)

- Multiply by 0.50, 0.30, 0.20 — write the three target dollar amounts down

- Pull last 3 months of bank/credit card transactions; categorize into the three buckets

- Compare actuals to targets — every category over budget is a flag, not a failure

- Pick ONE category to fix this month. Don’t try to overhaul everything.

- Re-check in 30 days

Is the 20% savings rate enough for retirement?

For most Americans starting in their 20s, yes — assuming you start early and stay consistent. The SEC‘s investor.gov compound interest calculator at a 7% real return (S&P historical average, not guaranteed) shows:

- Saving $750/month from age 25 to 65 = ~$1.97M

- Saving $750/month from age 35 to 65 = ~$913K

- Saving $750/month from age 45 to 65 = ~$391K

The most important variable is time, not amount.

FAQ

Q1. Is the 50/30/20 rule outdated in 2026?

The percentages are still useful as a starting framework. What’s outdated is applying them rigidly in HCOL cities. The principle — explicitly bucketing needs, wants, and savings — remains as relevant today as in 2005.

Q2. Does the 20% include my 401(k)?

Two valid approaches. (A) Calculate net AFTER 401(k) is taken out — then the 20% is additional savings on top. (B) Calculate net before 401(k) and count the 401(k) in the 20%. Pick one and stick with it.

Q3. What if I can only save 10%?

10% is better than 0%. The Federal Reserve‘s 2024 Survey of Consumer Finances showed median Americans saved 4–5%. Save 10% now and grow it 1% per year as your income increases.

Q4. Should student loans go in needs or savings?

Minimum payments = needs (the 50%). Anything you pay above the minimum = savings/debt payoff (the 20%). Same logic for credit cards and car loans.

Q5. What about taxes — do I include them in the 50%?

No. 50/30/20 runs on net (post-tax) income. Federal tax, FICA, and state tax are already gone before the rule even starts.

Related: monthly budget planner, saving $500/month on $40K, money-saving tips for American households.