I started taking budgeting seriously the year I began CFP® coursework. Every textbook chapter on cash-flow planning made the same point: most Americans budget on gross salary, not net — and that’s why budgets break in week two.

Here’s the system I’m using and teaching to friends, with actual US numbers for January 2026.

Step 1 — What’s your real take-home pay?

Don’t budget on your offer letter. Budget on the number that hits your checking account every two weeks.

For a $75,000 single filer in 2026, using IRS federal brackets and assuming a 6% 401(k) contribution:

- Gross: $75,000

- 401(k) 6%: −$4,500 (pre-tax)

- Health insurance premium (employee share, avg): −$1,500

- Standard deduction: −$14,600 → taxable $54,400

- Federal income tax (10% + 12% + 22% brackets blended): ~$7,420

- FICA (7.65% of $70,500 post-401k wages): ~$5,393

- State tax (avg ~4%, MA ~5%): ~$2,820 ($0 in TX/FL/WA/NV/TN/SD/WY/AK)

Net annual take-home: ~$53,367 → ~$4,447/month. That’s the number your budget runs on.

Step 2 — What buckets should the budget have?

The simplest split that survives contact with reality: three buckets.

- Fixed (must pay): rent/mortgage, car loan, insurance, utilities, subscriptions you actually use

- Variable (you control): groceries, dining, gas, fun money, clothes, gifts

- Savings + debt payoff: emergency fund, Roth IRA, extra 401(k), credit card payoff above minimum, sinking funds for big future expenses

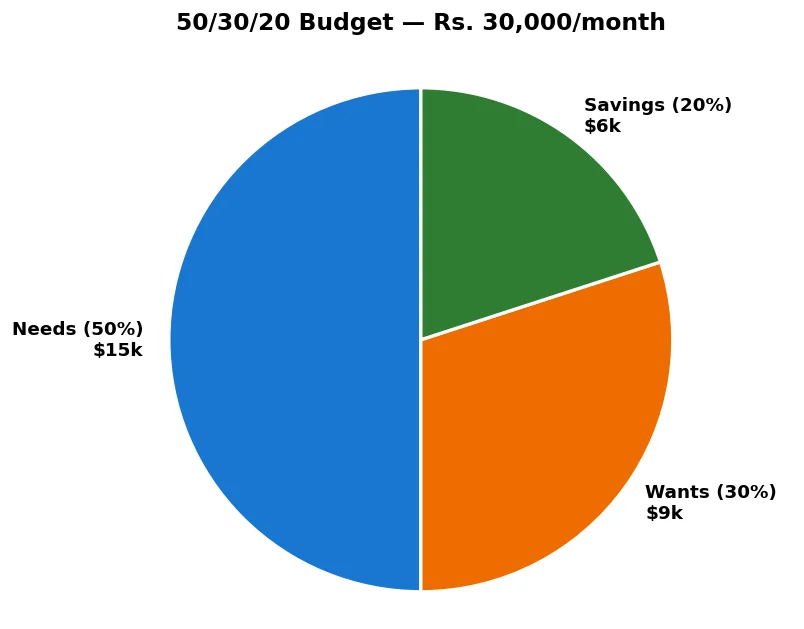

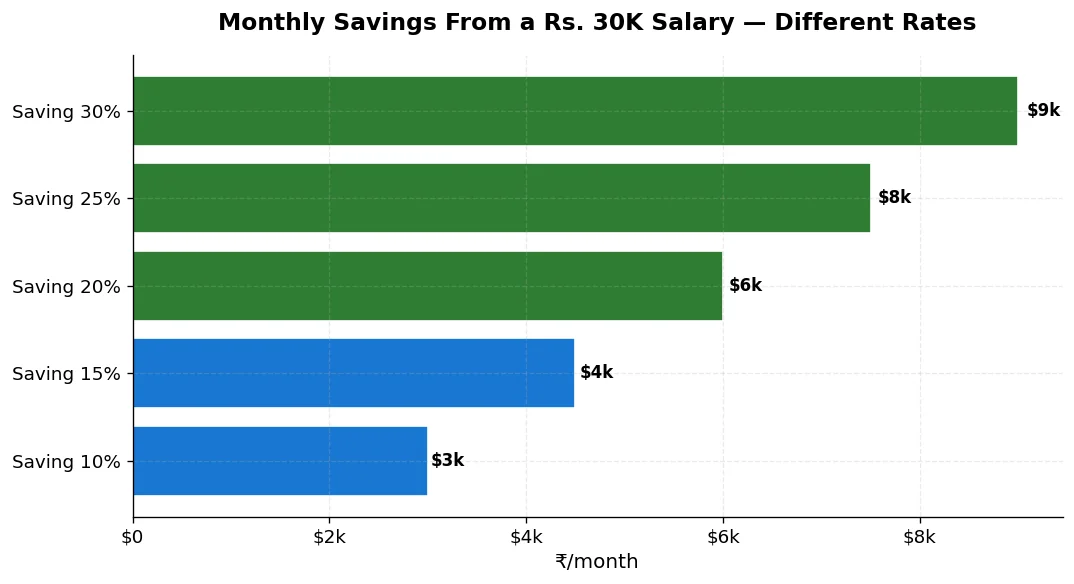

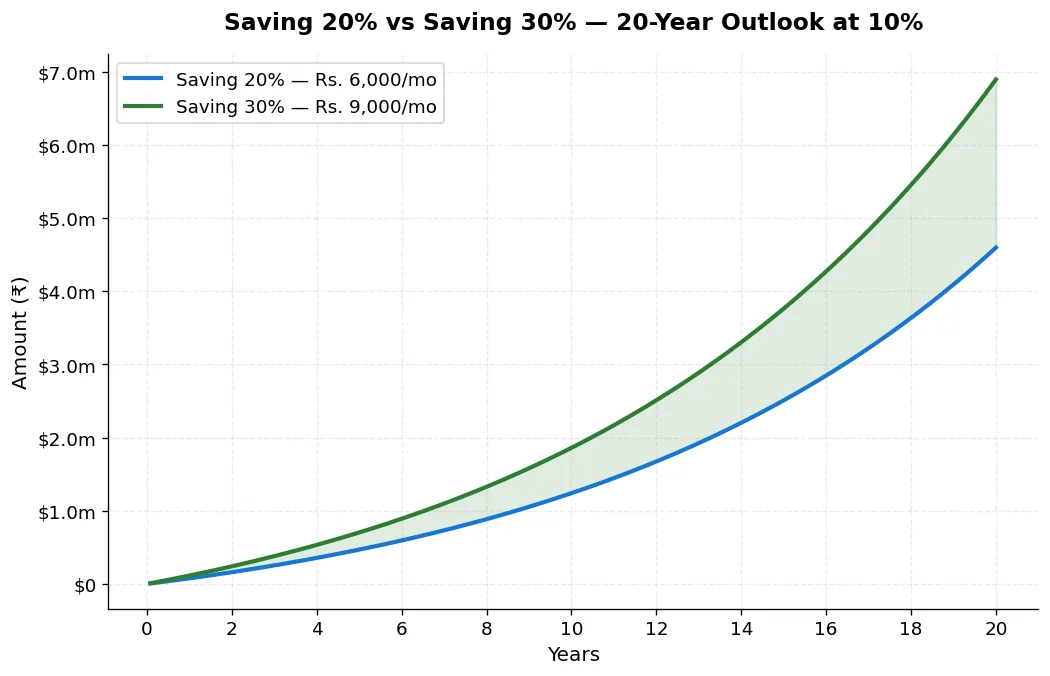

The popular 50/30/20 rule slots into this: 50% fixed needs, 30% variable wants, 20% savings/debt. I cover that in detail in my 50/30/20 explainer for US incomes.

Step 3 — What does the budget look like at $50K, $75K, $100K?

Approximate post-tax monthly take-home and a healthy 50/30/20 split (single filer, 6% 401(k), avg state):

| Gross | Net/mo | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|---|

| $50,000 | ~$3,150 | $1,575 | $945 | $630 |

| $75,000 | ~$4,447 | $2,223 | $1,334 | $890 |

| $100,000 | ~$5,810 | $2,905 | $1,743 | $1,162 |

Step 4 — How do you track for the first 30 days?

For one month, write down or app-log every single transaction. Yes, every coffee. The point isn’t shame — it’s catching leaks.

The first time I did this I found $47/month going to a Peacock + Disney+ bundle I hadn’t used since the holidays. Multiply that across 5 unused subscriptions and the average household leaks $200+/month per CFPB consumer research on subscription traps.

Which budgeting app should you use?

Mint (Intuit) shut down in early 2024. The current main options for Americans:

- YNAB — zero-based, $109/year, steep learning curve, best for control freaks

- Monarch Money — Mint’s spiritual replacement, ~$100/year, multi-account aggregation

- Rocket Money — free tier + premium, focused on canceling subscriptions and lowering bills

- Copilot Money — iOS only, $95/year, clean design

- Empower (formerly Personal Capital) — free for budgeting + net worth tracking

I cover trade-offs in my full 2026 budgeting app comparison.

What are the most common budget mistakes I’m avoiding?

- Forgetting irregular expenses — car registration, holiday gifts, Amazon Prime annual fee. Use a sinking fund for these.

- Budgeting gross instead of net — the #1 reason budgets break.

- No buffer category — leave 5–10% unallocated for the inevitable surprise.

- Reviewing only once a quarter — budgets need a weekly 10-minute check-in.

- Cutting fun to zero — guarantees the budget collapses in week three.

How do you adjust the budget every month?

At month-end, compare actuals to plan. For every category that overspent, ask: was it a one-time event (medical, car repair) or a pattern? If it’s a pattern, the budget is wrong — adjust the plan, don’t beat yourself up.

I do a 20-minute “money date” with myself on the first Sunday of every month. Coffee, spreadsheet, honest review. No apps required for this — just clarity.

Where does the savings bucket go?

Priority order while I’m studying for CFP — this is the conventional ordering taught in fee-only planning:

- Capture full 401(k) employer match (instant ~50–100% return)

- Pay off any debt above ~7–8% APR (credit cards, personal loans)

- Build a $1,000 starter emergency fund

- Max Roth IRA ($7,000/year in 2026 per IRS) if under income limit

- Grow emergency fund to 3–6 months expenses

- Increase 401(k) toward the $23,500 employee max

- Taxable brokerage for goals beyond retirement

FAQ

Q1. Should I use percentages or dollar amounts?

Both. Set percentage targets (50/30/20) for direction, but plug in real dollar amounts each month. Percentages help you scale the budget as your salary grows; dollars keep you honest week-to-week.

Q2. How is a US budget different from countries with universal healthcare?

Health insurance, copays, HSA contributions, and out-of-pocket maximums are huge US-specific line items. Per HealthCare.gov, average employer-sponsored single coverage premium employee share is ~$1,500/year in 2026 — and that’s before deductibles.

Q3. Do I include 401(k) in the savings 20%?

Yes — pre-tax 401(k) counts. Most people budget on net pay (after 401(k) is already deducted), so the 20% is additional after-tax savings. Either approach works as long as you’re consistent.

Q4. What about variable income (1099, freelance, commission)?

Budget against your minimum reliable month, not your average. Treat anything above the minimum as bonus → straight to savings or estimated taxes. Set aside 25–30% of every 1099 payment for federal + state quarterly taxes per IRS guidance.

Q5. How long before a budget actually works?

Honest answer: 3 months. Month 1 = chaos and discovery. Month 2 = first real adjustments. Month 3 = you have a working baseline. Anyone who quits after one month never finds out the system works.